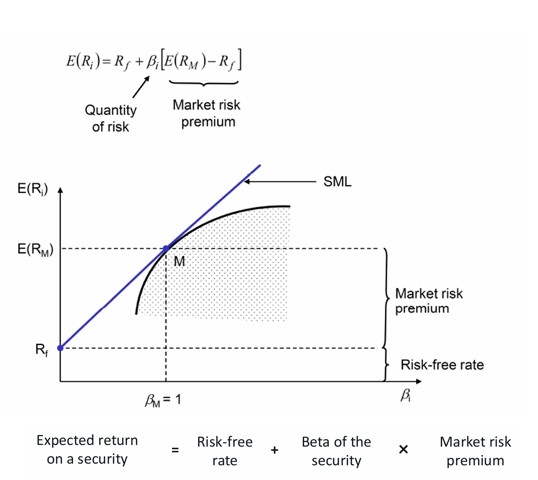

1) Why SML & Beta Are Important

The Security Market Line (SML) links an asset’s expected return to its exposure to systematic (market) risk, measured by beta. Its intercept is the risk-free rate and its slope is the market risk premium. You use the SML to estimate the cost of equity, to check for alpha (over/undervaluation), and to compare strategies on a consistent, risk-adjusted basis.

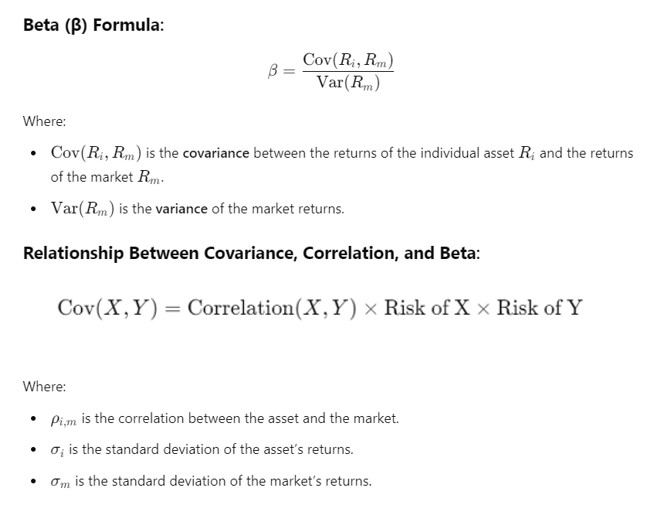

2) What Is Beta?

Beta (β) measures how sensitive an asset’s return is to movements in the market portfolio. In words: if the market moves by 1%, beta indicates how much the asset typically moves in response.

- β ≈ 1: market-like sensitivity.

- β > 1: aggressive; amplifies market moves.

- β < 1: defensive; dampens market moves.

- β ≈ 0: largely uncorrelated with the market.

- β < 0: tends to move opposite the market.

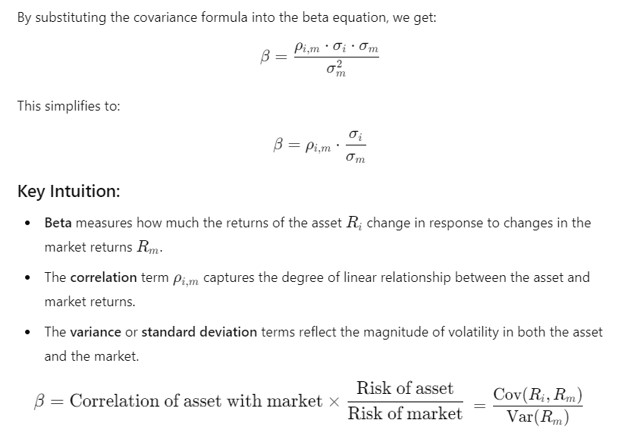

3) Relationship Between Covariance, Correlation, and Beta

Beta comes from co-movement with the market. Conceptually, it grows when two things rise: the tightness of the relationship between the asset and the market (correlation), and the asset’s volatility relative to the market.

- Co-movement idea: the stronger and more consistent the asset’s tendency to move with the market, the larger its beta.

- Relative scale: even a volatile asset can have a small beta if it rarely moves with the market; conversely a moderate-volatility asset can have a high beta if it tracks the market closely.

- Bounds intuition: beta cannot explode simply from noise; it is anchored by both the strength of the relationship and the relative variability of the asset and the market.

If you want to show the algebra later, add your own images for the covariance form, the correlation form, and the regression form that defines the slope.

4) Market Beta and Portfolios

- Market portfolio: by construction has a beta of one.

- Portfolio beta: equals the weighted average of the component betas.

- Leverage effect: borrowing to hold more of a portfolio scales its beta up; holding some cash scales it down.

- Risk-free asset: has beta of zero; mixing it with risky assets adjusts portfolio beta linearly.

5) Interpreting Beta on the SML

- Required return: higher beta implies a higher return is required to compensate for market risk.

- Alpha check: compare an asset’s expected (or realized) return to the SML at its beta. Above the line suggests positive alpha; below suggests negative alpha.

- Cost of equity: plug a project or firm’s beta into the SML to obtain a discount rate consistent with market risk.

- Measurement notes: betas can change over time and are estimated with error; use sensible windows, peer comparisons, and leverage adjustments.

6) Sensitivity Examples and How β Is Used

The sensitivity of changes in a firm’s share price to general market movements:

- β = 1.2: if the market rises by 10%, the stock is expected to rise by about 12% on average; if the market falls by 10%, the stock is expected to fall by about 12% on average.

- β = 0.6: if the market rises by 10%, the stock is expected to rise by about 6% on average (and similarly in downturns).

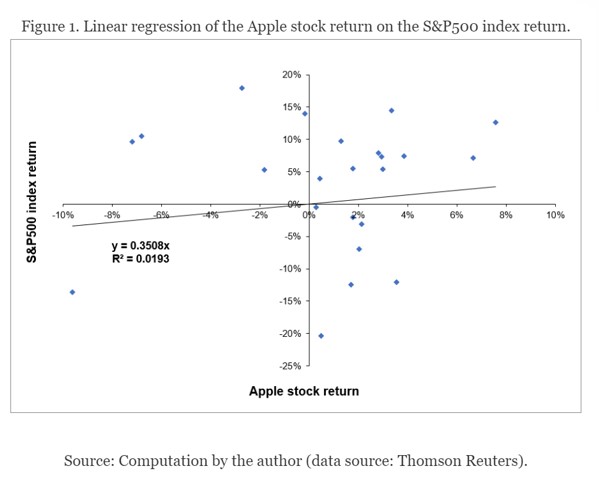

- Example estimate: an estimated beta of 0.3508 lies between zero and one, indicating the stock tends to fluctuate less than the market index.

What β Measures (Summary)

- Systematic risk: the non-diversifiable component tied to economy-wide factors.

- Sensitivity: typical percentage response of the asset to a one-percentage-point change in the market’s return.

- Covariation: the degree to which the asset and market move together, scaled by the market’s variability.

| Beta level | Typical behavior vs market | Common label |

|---|---|---|

| β > 1 | Magnifies market moves (↑ risk, ↑ required return) | Aggressive |

| β ≈ 1 | Moves roughly with market | Market-like |

| 0 < β < 1 | Moves with market but less so | Defensive |

| β ≈ 0 | Little relation to market | Uncorrelated |

| β < 0 | Tends to move opposite the market | Hedge-like |